The Eroding Dollar: Why Advisors Need a New Playbook for Client Portfolios

For decades, financial advisors have told clients that careful diversification, patience, and discipline are keys to retiring securely. Money once meant safety. Bonds once meant income stability – the foundation of retirement income. Today, that bedrock is cracking under the weight of inflation and a dollar in decline. A primary source of retirement income – bond portfolios – have generated negative returns after inflation over the past decade. No wonder many clients don’t feel better off. The problem is that almost every investment plan begins with the same assumption: the U.S. dollar, the world’s reserve currency, holds its worth.

A Decade of Negative Real Returns: Bonds Have Failed to Protect Purchasing Power1

Nominal returns disguise real losses once inflation is accounted for.

1 Bloomberg LP. Bond portfolios represented by the Bloomberg U.S. Aggregate Bond TR Index, which is a broad-based fixed income index that represents the overall performance of the U.S. investment grade bond market, including U.S. Treasurys, corporate bonds, mortgage-backed securities, and asset-backed securities (excluding high yield or “junk” bonds). Cumulative Inflation represented by the Consumer Price Index, which is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. Data from 09/30/15 to 09/30/25. September 2025 CPI based on Bloomberg survey of economists.

Fiscal Policy’s Breaking Point

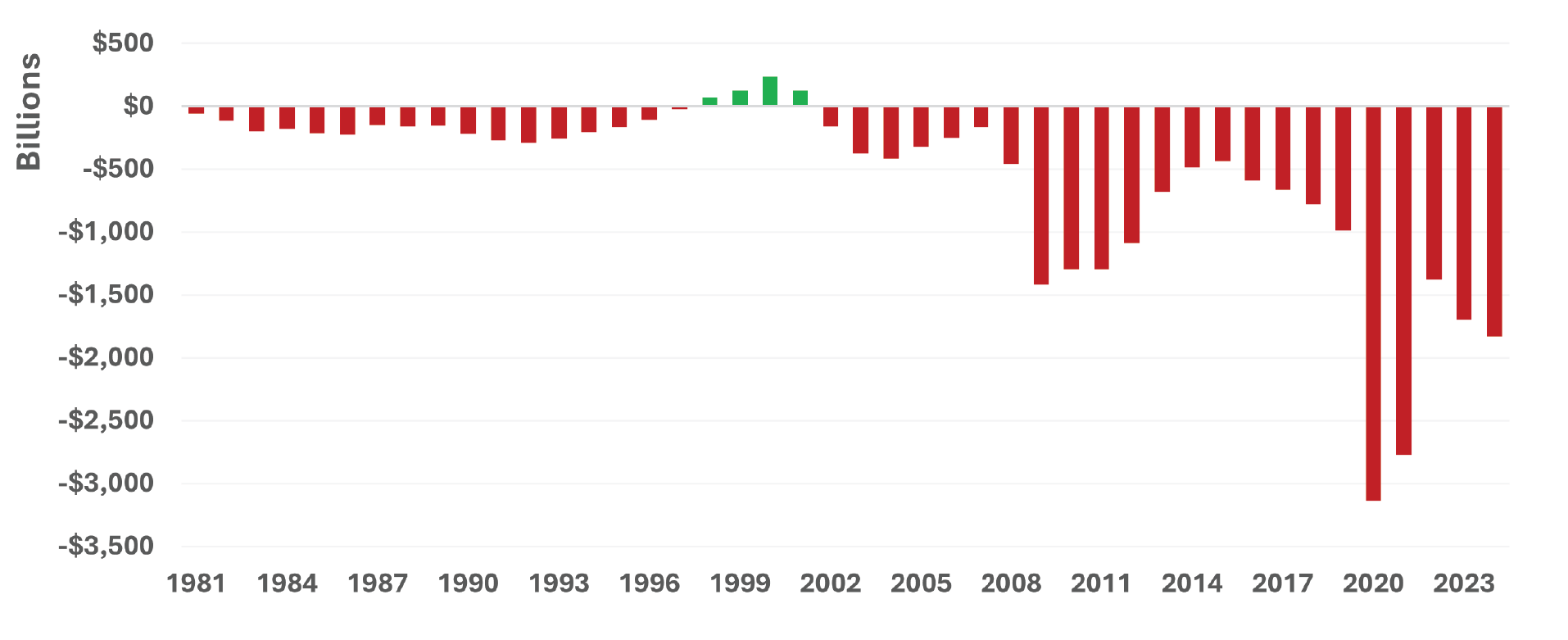

Deficits aren’t new, but trillion-dollar shortfalls are now an annual occurrence, driving a debt trajectory without precedent. For advisors, this isn’t abstract policy, it’s the silent force undermining every client’s real return.

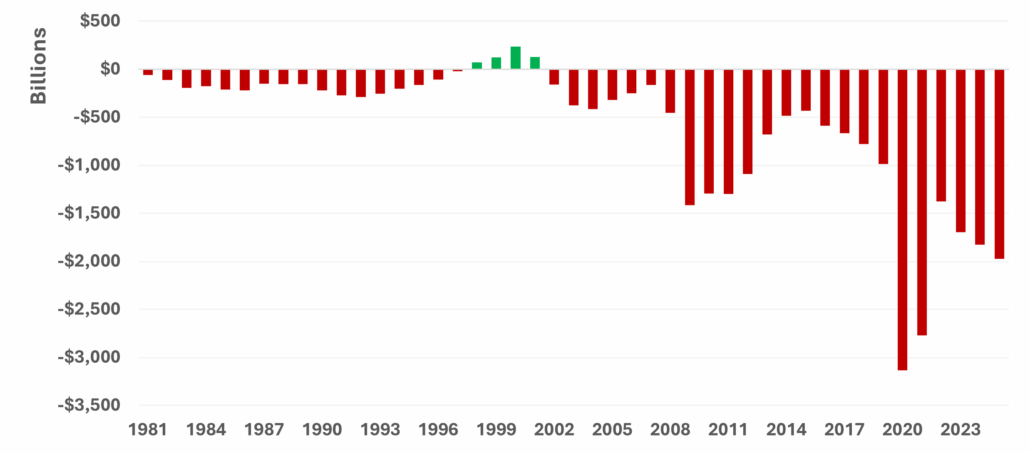

The U.S. Government Budget Deficit Has Become a Perpetual Crisis2

Trillion-dollar shortfalls have become a seemingly permanent feature of fiscal policy.

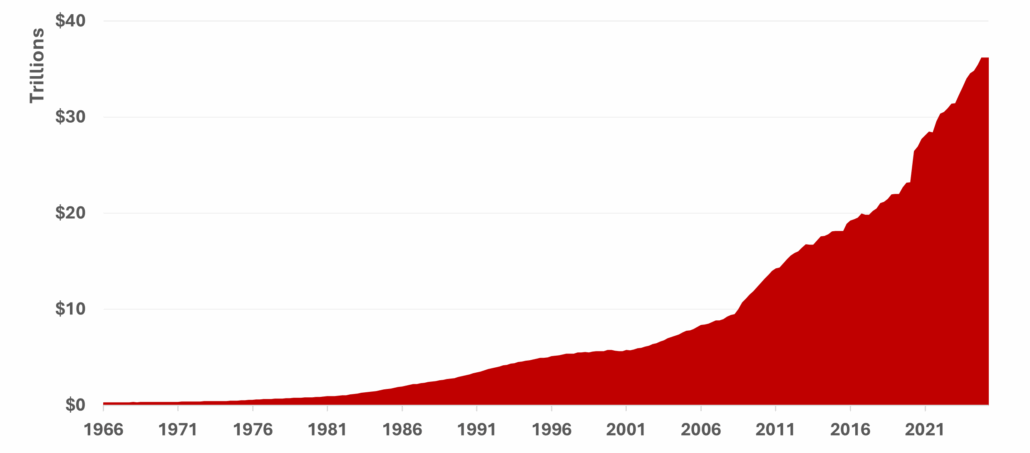

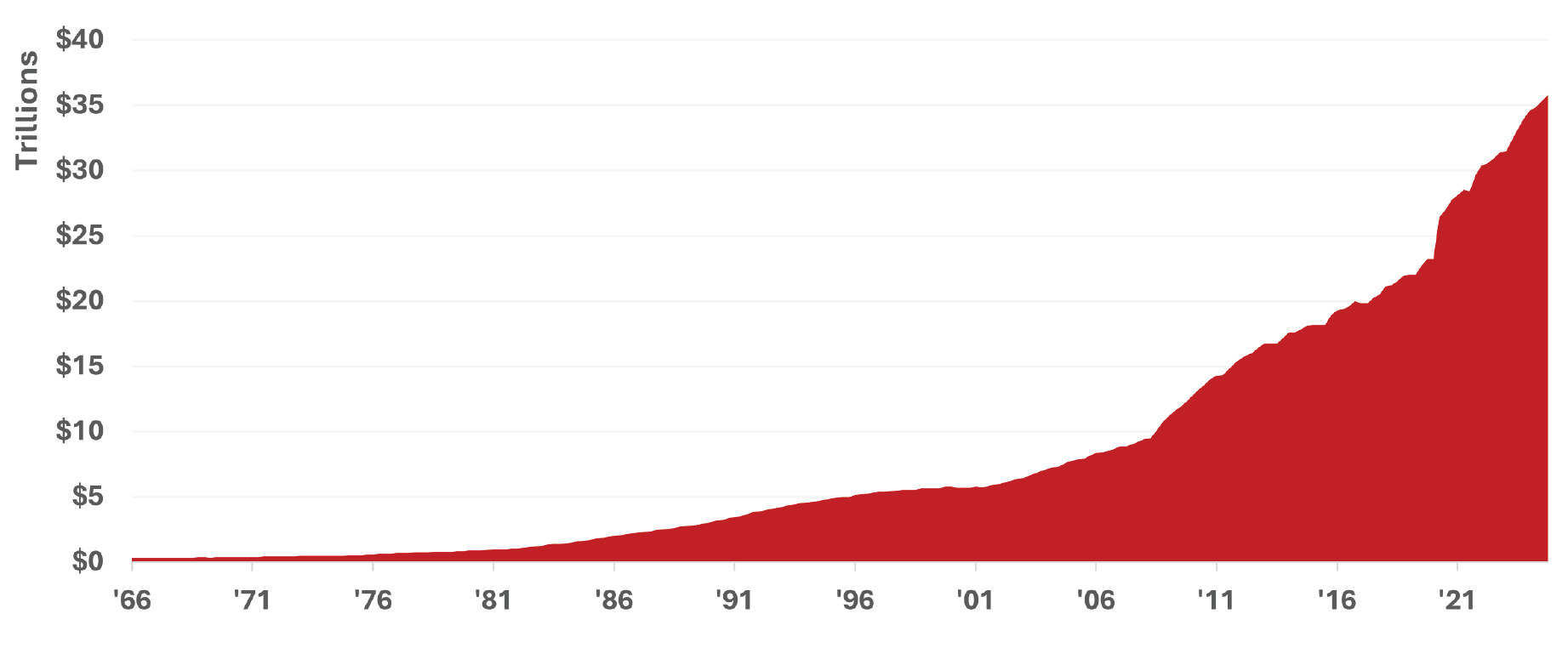

National Debt Has Grown Exponentially, Outpacing Economic Reality3

Growth in the national debt now exceeds the nation’s productive capacity

2U.S. federal deficit or surplus. U.S. Department of Treasury. Federal Reserve Economic Data. Based on monthly data through September 2025.

3Department of Treasury. Debt held by the public. Based on quarterly data through April 2025.

The Uncomfortable Truth: Washington’s Easiest Path Forward is Devaluation

Why are financial advisors finding a disconnect between market performance and client experience? Grocery bills are up +20%4, and “safe” instruments like CDs are paying far less than that. Even traditional investments, like bonds, are down after inflation. Clients can feel the math – and they’re right. The dollar simply buys less.

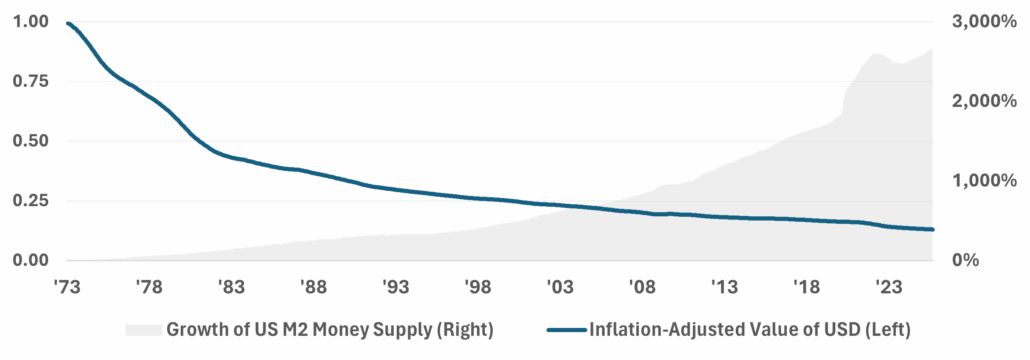

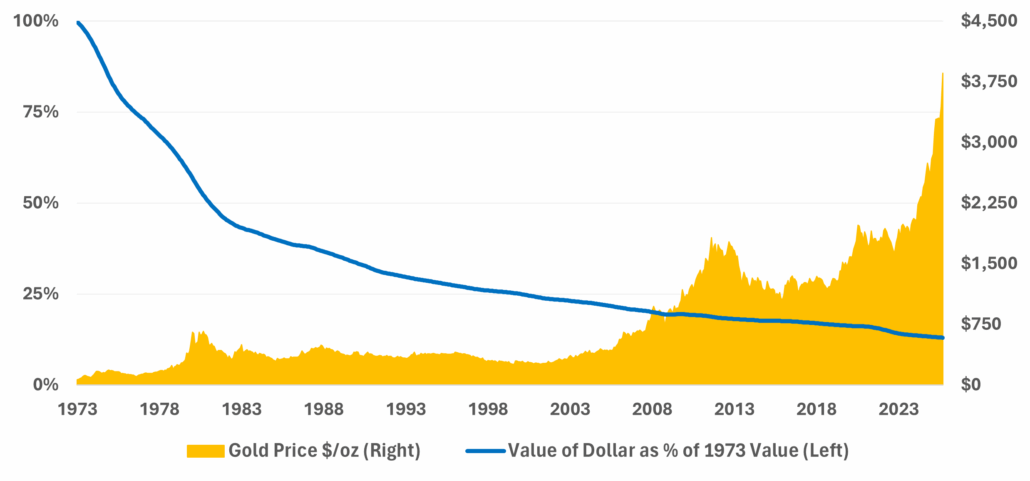

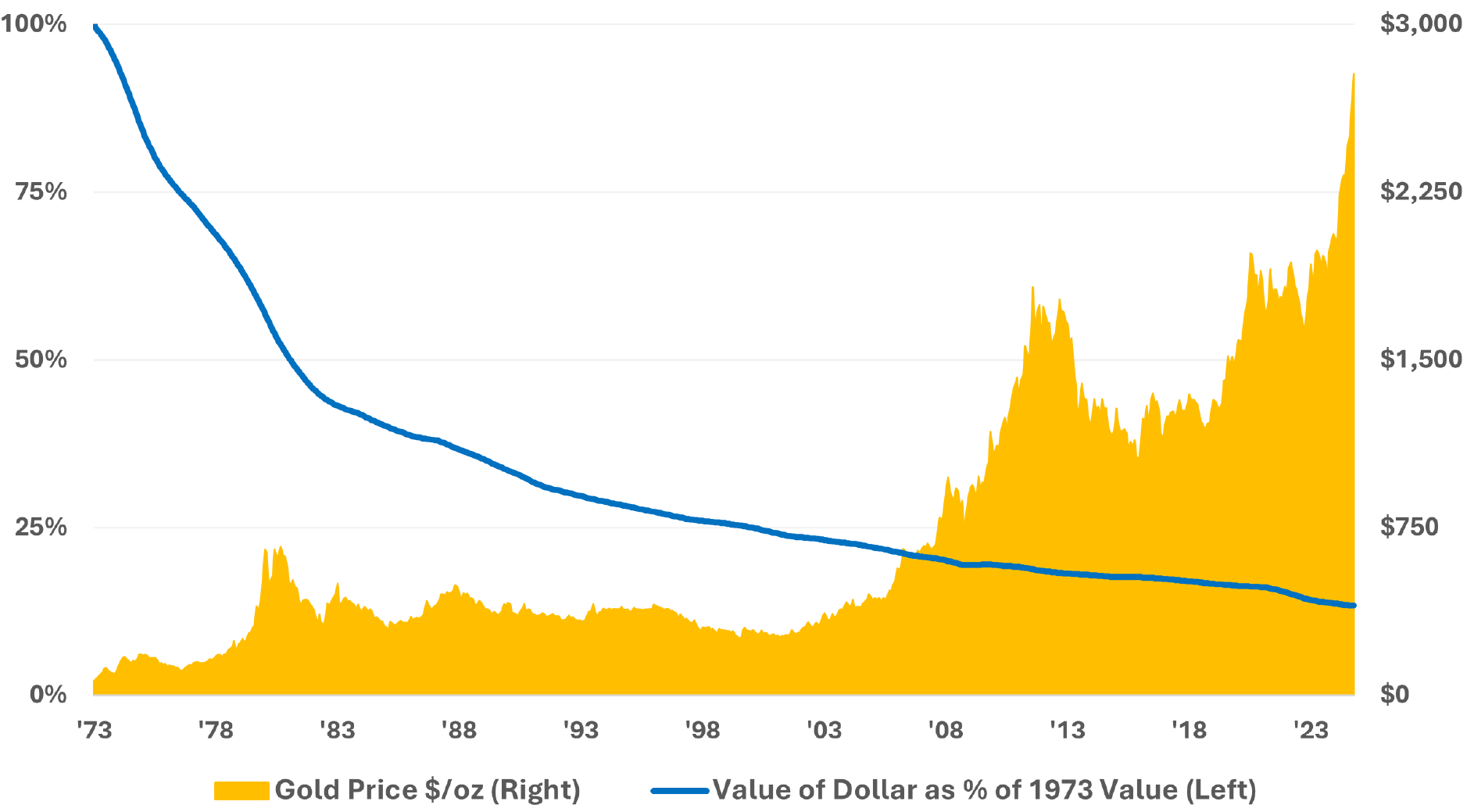

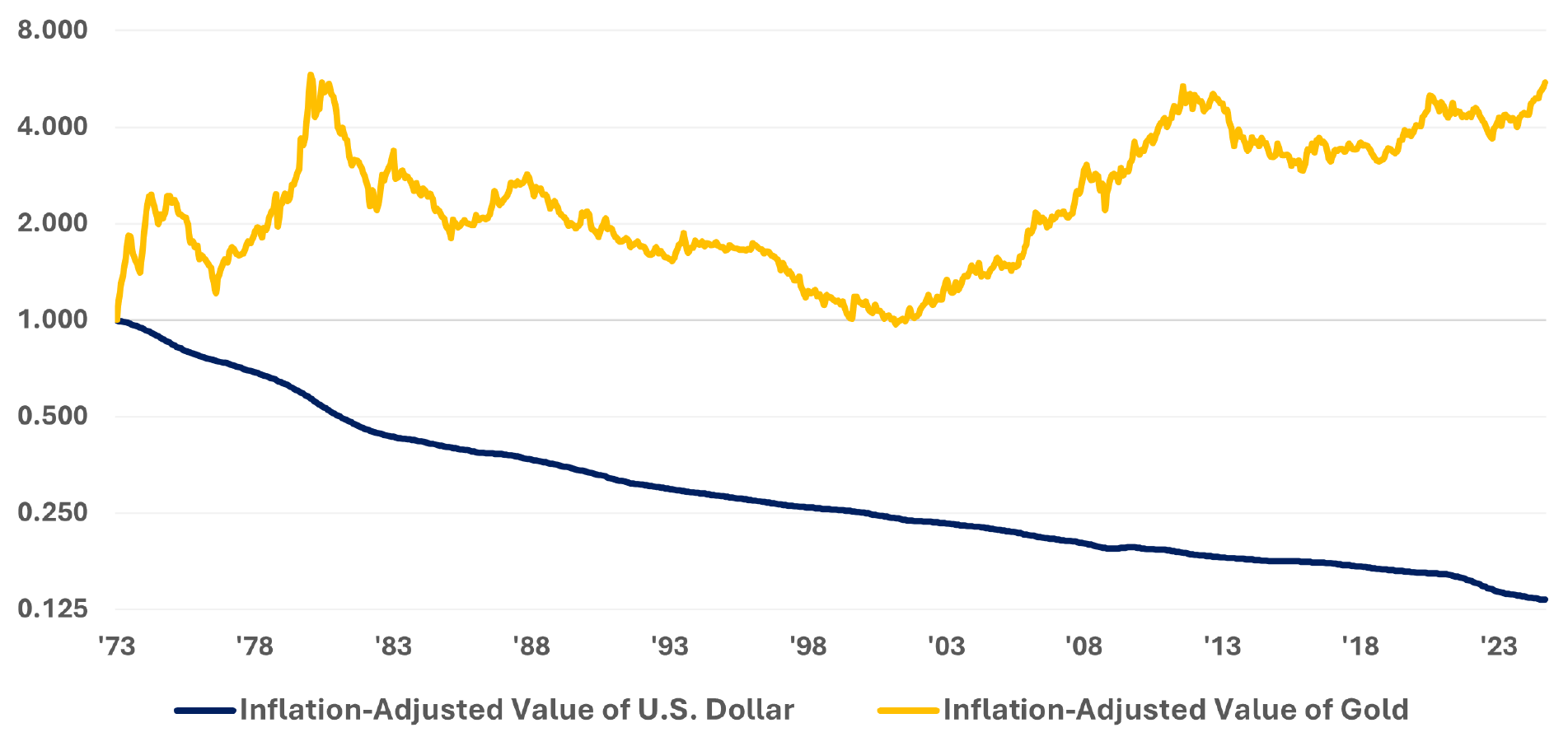

The purchasing power of the dollar is declining. The long-term chart of the dollar’s purchasing power dating back to 1973 shows a significant decline. What once bought a cart of groceries in 1973 could barely buy a bag of groceries today. A dollar is worth just 13 cents of what it used to be.

Decades of excessive spending by the federal government and easy monetary policy by the Federal Reserve have flooded the economy with dollars faster than it can produce goods and services, diluting purchasing power and feeding inflation.

How do you service $1 trillion in debt when there’s no fiscal room left? Simple, you print more money and continue to devalue the dollar. Inflation has already erased a decade of real bond returns. Fiscal devaluation isn’t a failure, it’s the plan.

When policy rewards spending over saving, the dollar itself becomes the casualty.

By the numbers

A system built to spend money, not save.

Every U.S. Dollar Printed Buys Less6

The money supply has risen nearly 200% since 2008. A growing supply of dollars chases the same goods: the recipe for inflation.5

4Source: U.S. Bureau of Labor Statistics. Data for 2025 compared to 2020.

5M2 money supply is a measure of money circulation that includes total dollars in cash deposits and other deposits readily convertible to cash, such as money market funds.

6Bloomberg LP. Board of Governors of the Federal Reserve. OECD. September 2025.

7U.S. Department of Treasury. September 2025.

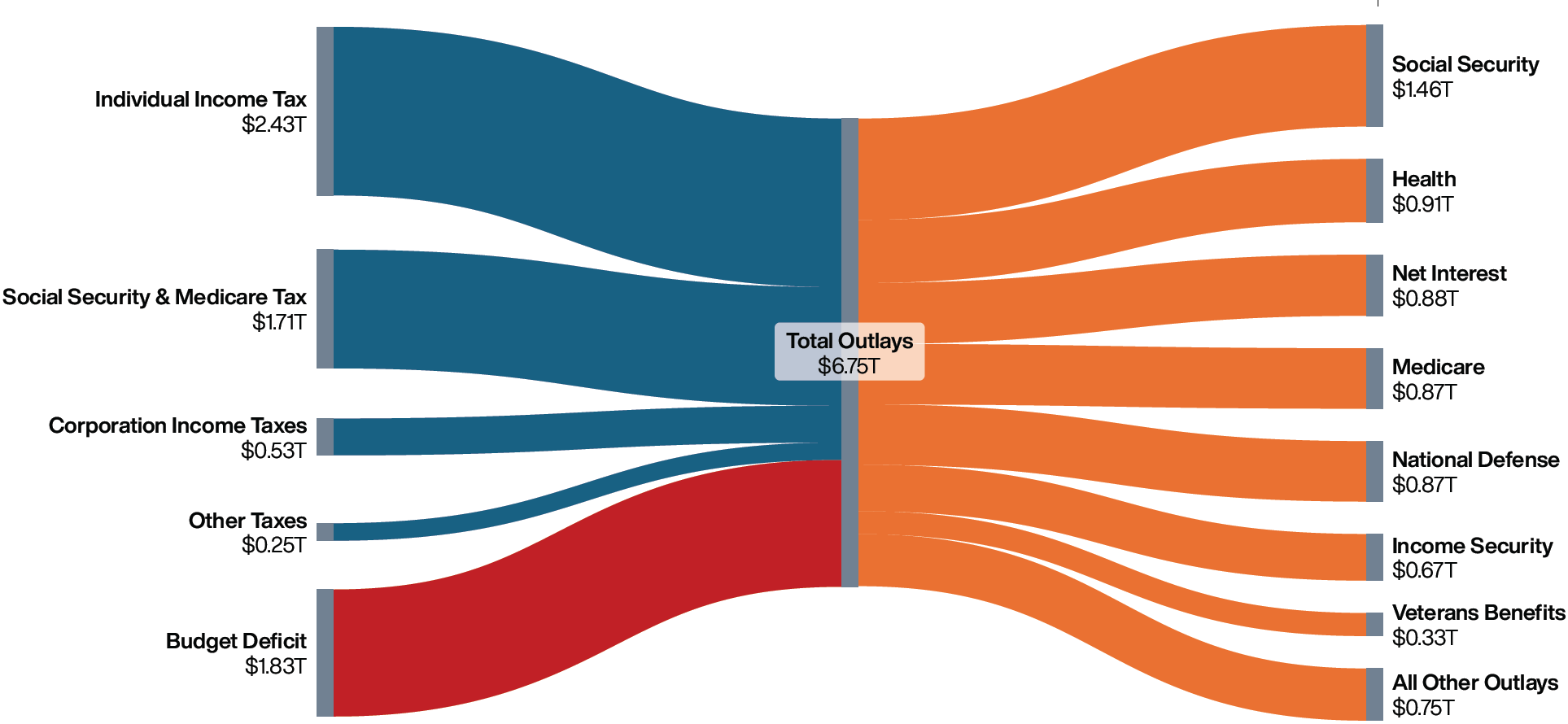

Washington Spent $1.78 Trillion More Than It Earned in 2025 – Again8

When spending outpaces revenue this dramatically, inflation becomes policy.

De-Dollarization Isn’t Rebellion, It’s Recognition

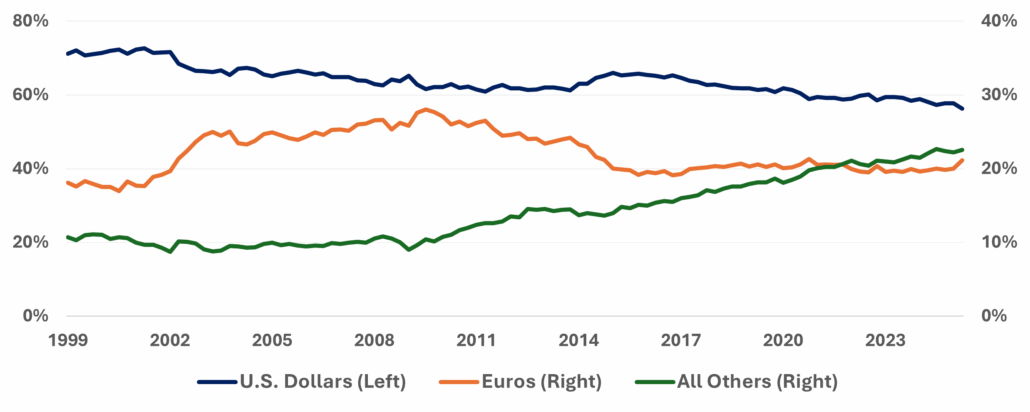

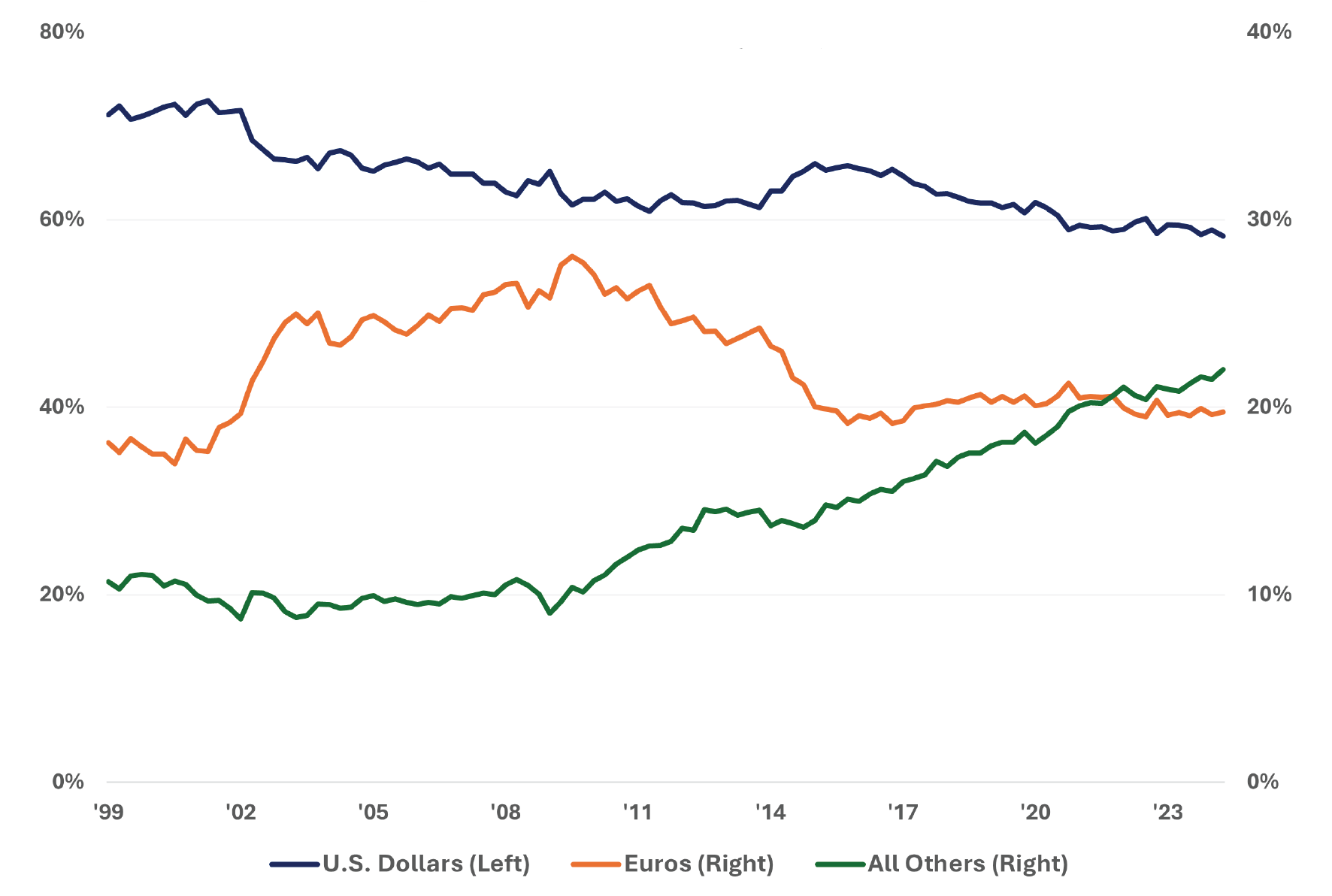

What Washington treats as a domestic problem, the rest of the world now treats as a risk to avoid. The rest of the world is acting on what Washington refuses to admit. Amid rising U.S. debt and persistent geopolitical tensions, central banks have quietly reduced their U.S. dollar exposure, putting further downward pressure on the dollar’s value. For the first time in a generation, global reserve managers are voting with their reserves, and not with the dollar.

- The U.S. dollar’s share of global reserves has dropped from 71% in 1999 to 56% today.

- Foreign holdings of U.S. debt have dropped by almost a third.

Fiscal devaluation isn’t a failure. It’s the plan.

U.S. Dollar as a % of FX Reserves: Global Confidence in the Dollar Is Fading9

The dollar’s share of global reserves has fallen from 71% in 1999 to 56% today.

8U.S. Department of Treasury. September 2025.

9Bloomberg LP. IMF COFER. June 2025.

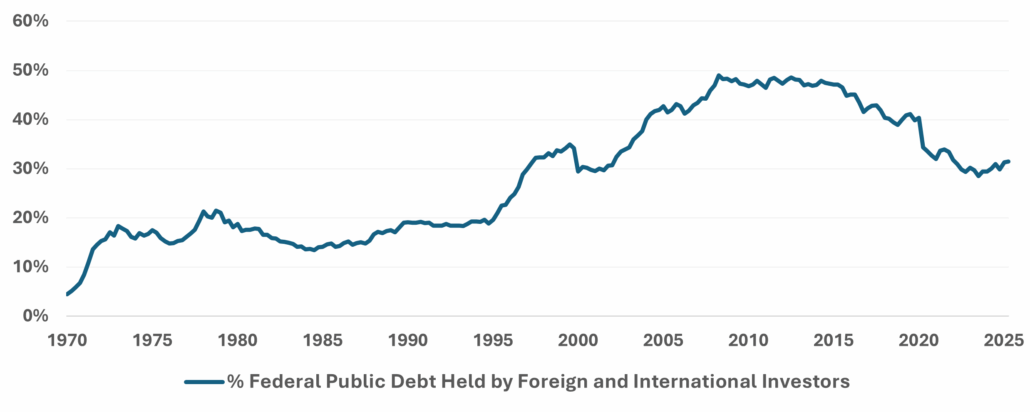

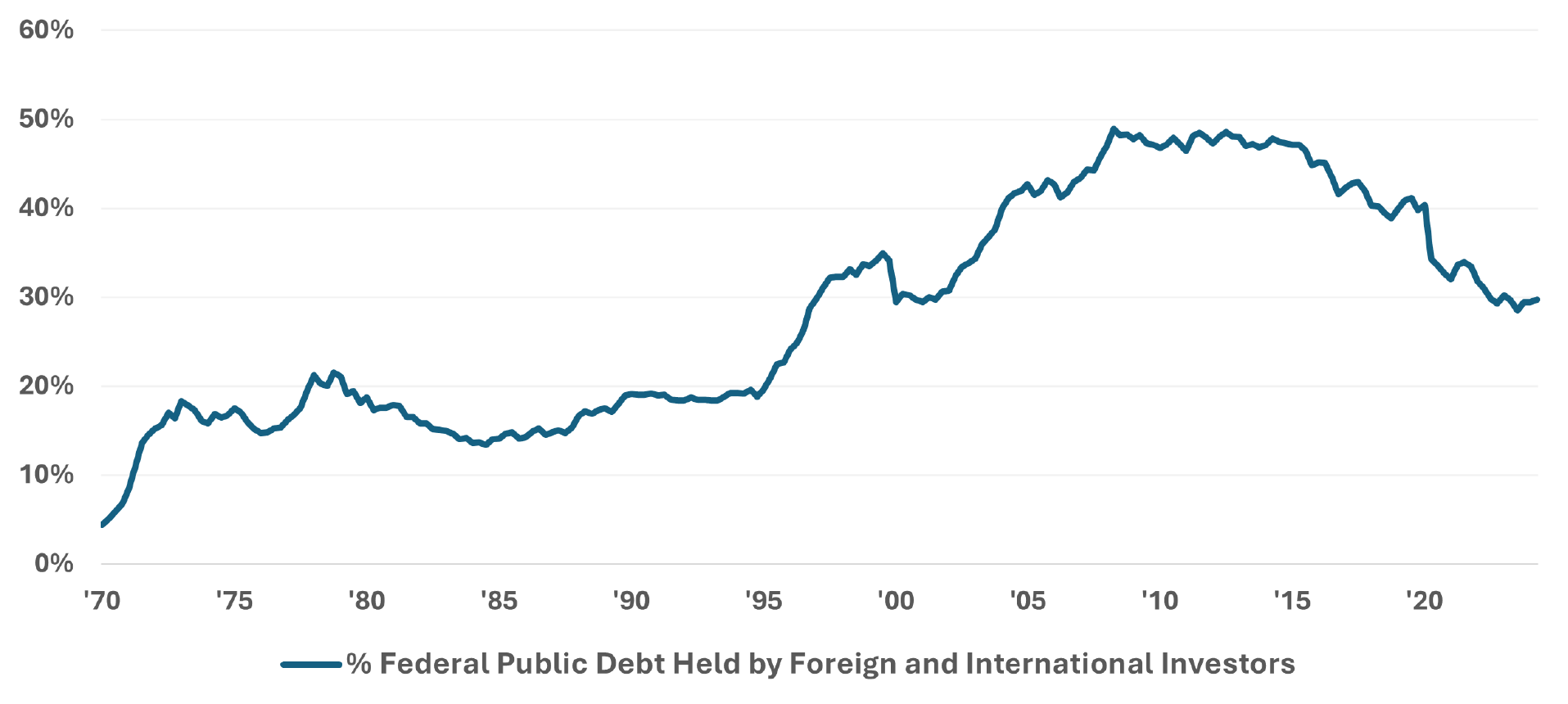

Foreign Investors Are Turning Away from U.S. Debt, and That’s Not Good For the Dollar10

Foreign ownership of U.S. debt has dropped from nearly 50% to just over 30% since 2008.

Gold: The Asset That Doesn’t Lie

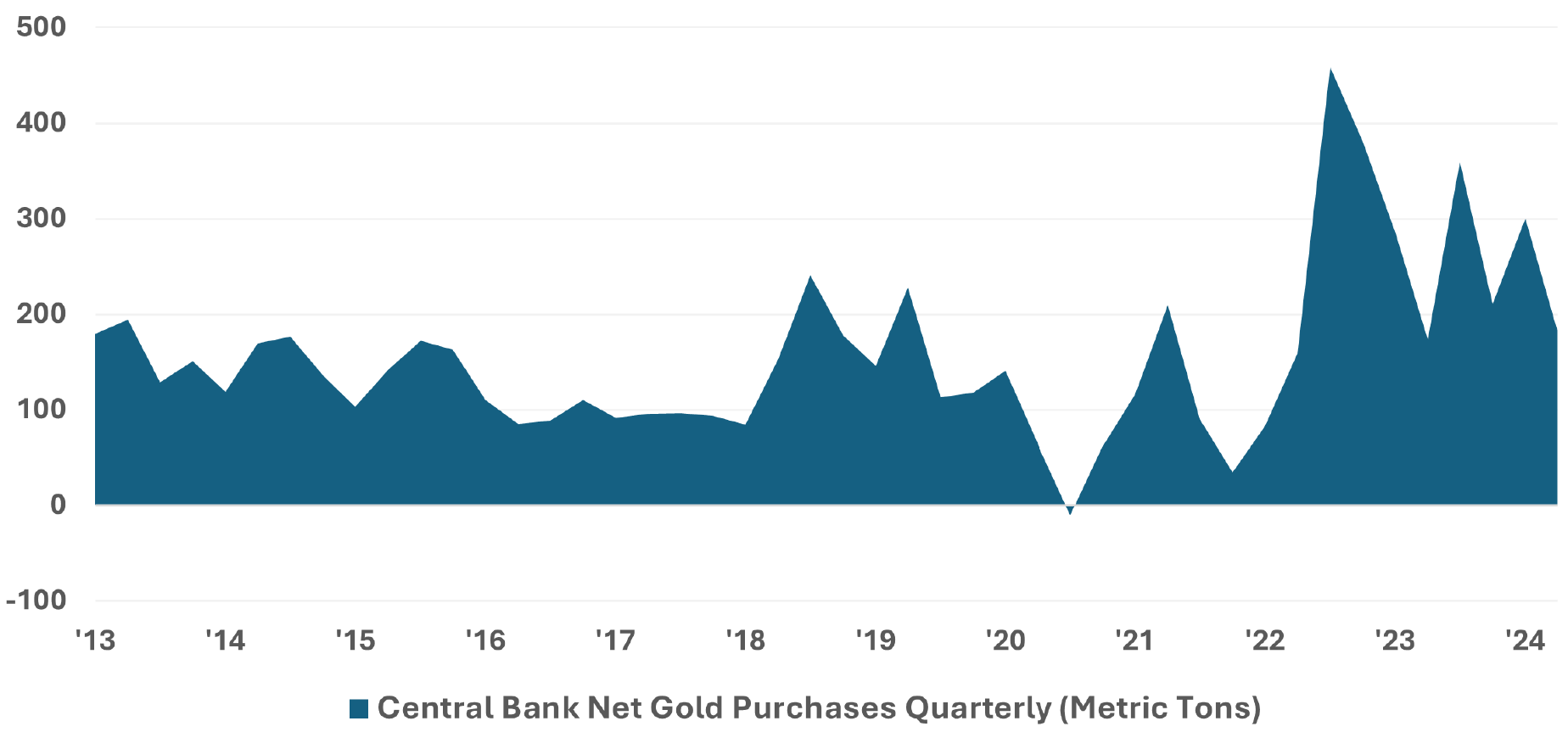

In the 1970s, gold soared as the dollar broke from its anchor.11 Today, central banks are restoring that anchor, not for nostalgia, but necessity. Nations around the world are making record purchases of gold. It’s driven by math as much as by geopolitics. Nations are essentially hedging against policy failure.

- From March 2013 to March 2022, global central banks made net gold purchases of 126 metric tons per quarter, on average.

- From June 2022 to September 2025, these net purchases increased to an average of 269 metric tons per quarter.

A Global Shift: Central Banks Double Gold Buying Since 202212

The world’s monetary authorities are trading paper promises for a tangible store of value in gold.

10U.S. Department of Treasury. April 2025.

11Prior to 1971, the U.S. dollar was backed, at least in part, by gold reserves (commonly referred to as the “gold standard”). In 1971, the U.S. switched to a fiat monetary system, effectively ending the “gold standard.” Fiat money has no value of its own and is not backed by gold; rather, its value is derived from the trust and stability of the government that issues it.

12Bloomberg LP. Quarterly demand (net purchase) data. September 2025.

Global confidence in the dollar is fading — not suddenly, but steadily.

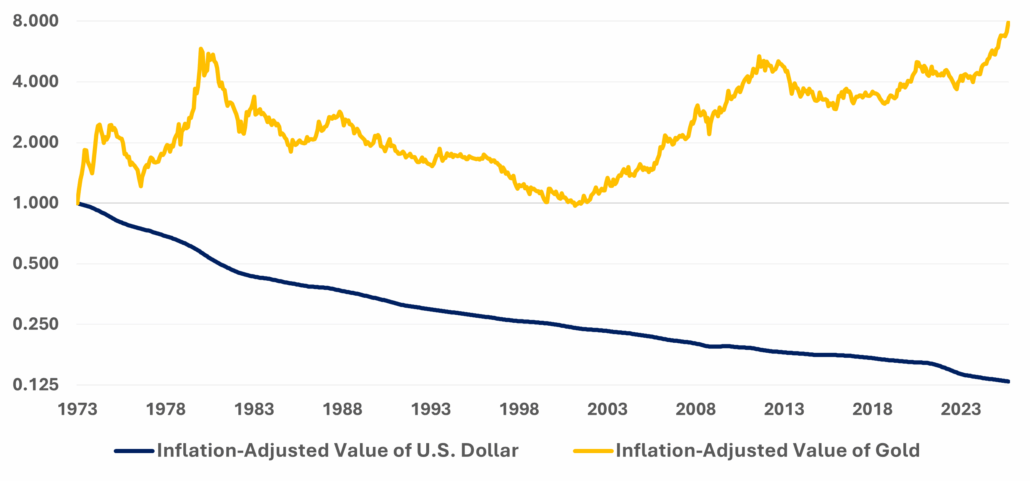

The desire for gold should come as no surprise. When looking at a chart since 1973 – the decade the dollar and gold parted ways – the value of gold has increased more than 60x (and almost 8x when adjusting for inflation). Half a century of data confirms gold’s role as a long-term store of value against monetary decay.

Fifty Years, One Story: Gold Preserved Value as the Dollar Lost It13

For half a century, gold has done what the dollar promised to do: hold its value.

The Asset That Kept Its Promise: After Inflation, Gold Still Wins14

Gold has delivered positive real returns across decades of shifting policy regimes.

Since 1973, gold has generally outpaced inflation. Its purchasing power has endured while fiat currencies have come and gone. Now, even the world’s largest central banks are accumulating gold again.

13Bloomberg LP. Board of Governors of the Federal Reserve. OECD. September 2025.

14Bloomberg LP. OECD. September 2025.

Gold Isn’t Fear, It’s Discipline

The U.S. government can’t cut spending without risking a collapse in confidence. So, it will likely take the easier road and let inflation do the work, whether it be official policy or not. The result will be that every dollar will buy a little less each year; not a typical immediate crisis, but rather a long-term process. Those who wait may be too late.

The role of the advisor isn’t to calm the storm; it’s to build an ark and make sure it floats as the flood of dollar devaluation continues to rise. It is difficult for clients to diversify away from Washington’s fiscal math, but they can own something that isn’t bound by it. An allocation to gold can be a fundamental part of the ark.

By positioning clients in gold, financial advisors offer the potential to defend purchasing power. Making modest allocations to gold isn’t about timing markets; rather, it’s about anchoring wealth to something real. Real wealth is measured by what endures when paper promises don’t, not necessarily just what your account statement tells you.

In a world where yield alone can’t buy stability, gold restores value-driven discipline to the modern income portfolio, offering the potential to protect purchasing power when it’s under the greatest attack. By combining gold with income producing assets, investors may be able to hedge their income against inflation. This design seeks to avoid the decline in purchasing power that continues to burden many.

Those who treat gold as a mere “trade” risk will miss its purpose; those who treat it as value-driven discipline are typically better able to preserve real wealth over time.

The role of the advisor isn’t to calm the storm; it’s to build the ark

Advisor Playbook Summary

- Inflation isn’t merely an economic cycle, it is increasingly a fiscal policy.

- Bonds no longer adequately defend income on their own.

- Gold isn’t just for speculation, it’s equally about wealth preservation and should be considered a value-driven discipline in physical form.

- A small allocation has the potential to make a lasting difference.

Is This the End of the Dollar as the World’s Reserve Currency?

Key Takeaways

According to Milton Friedman, there are four ways to spend money: spending your money on yourself, spending your money on someone else, spending someone else’s money on yourself, and spending someone else’s money on someone else. Why is this important? Because this construct helps explain how we went from the U.S. dollar securely holding the position of the world’s reserve currency to where it seems to be a matter of when, and not if, it will lose that status.

Prior to the 1970’s, the U.S. government historically operated with some degree of fiscal responsibility, partially because of the requirements under the Bretton Woods System (“BWS”) where the dollar was fixed to the price of gold. BWS dissolved between 1968 and 1973, and, by 1973, all major currencies began to float against each other1. In this free-floating system, the USD retained its status as the world’s reserve currency, leveraging the historical standard it had under BWS in the post-war era.

In the absence of fiscal constraints, like pegging the dollar to gold, it became clear that the U.S. government was spending someone else’s money — with little care and by printing as much as it could without risking the reserve currency status. As the years went on, the debt-financed deficits became more extreme and increasingly politically motivated. No end is in sight. De-dollarization has already started and is likely to continue.

In this environment, it comes as no surprise that gold continues to make headlines, whether from large central bank purchases, to record prices, to individuals buying up all the gold bars that Costco can stock. Gold is uniquely positioned to retain its value even in the face of extreme fiscal irresponsibility. In this white paper, we make the argument for why investors should hold gold and why gold is well positioned to replace the U.S. dollar as the world’s hard reserve currency.

Since the end of the Bretton Woods System, the dollar has tanked while gold surged2

1International Monetary Fund. The end of the Bretton Woods System (1972-81).

2Bloomberg LP. Board of Governors of the Federal Reserve. OECD. September 2024.

U.S. GOVERNMENT BUDGET DEFICITS AND DEBT ISSUANCE

To understand the driving factors behind the decline in the value of the dollar and the surge in the price of gold, one of the best places to start is by reviewing the fiscal policy of the U.S. government

The U.S. government spent $1.83 trillion more than it brought in during 20243

Following the end of BWS, the U.S. federal government was able to run a deficit with limited consequences. This accelerated over time to astronomical levels of spending following the great financial crisis in 2008.

There is usually a budget deficit and in 2024 it grew to the highest ex-pandemic level4

3U.S. Department of Treasury. September 2024.

4U.S. federal deficit or surplus. U.S. Department of Treasury. Federal Reserve Economic Data. Based on monthly data through September 2024.

So how does the government continue to operate if it is consistently spending more than it brings in? It issues debt by selling Treasurys and other securities.

Years of budget deficits have ballooned U.S. national debt to almost $36 trillion5

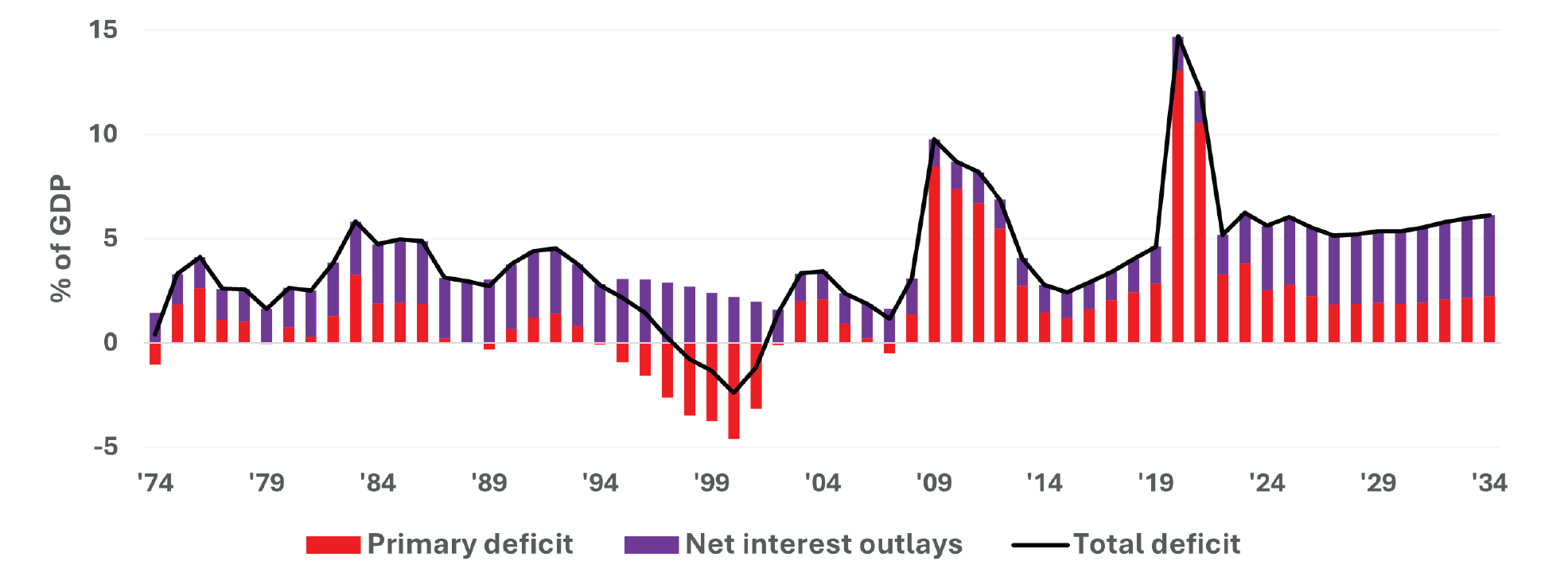

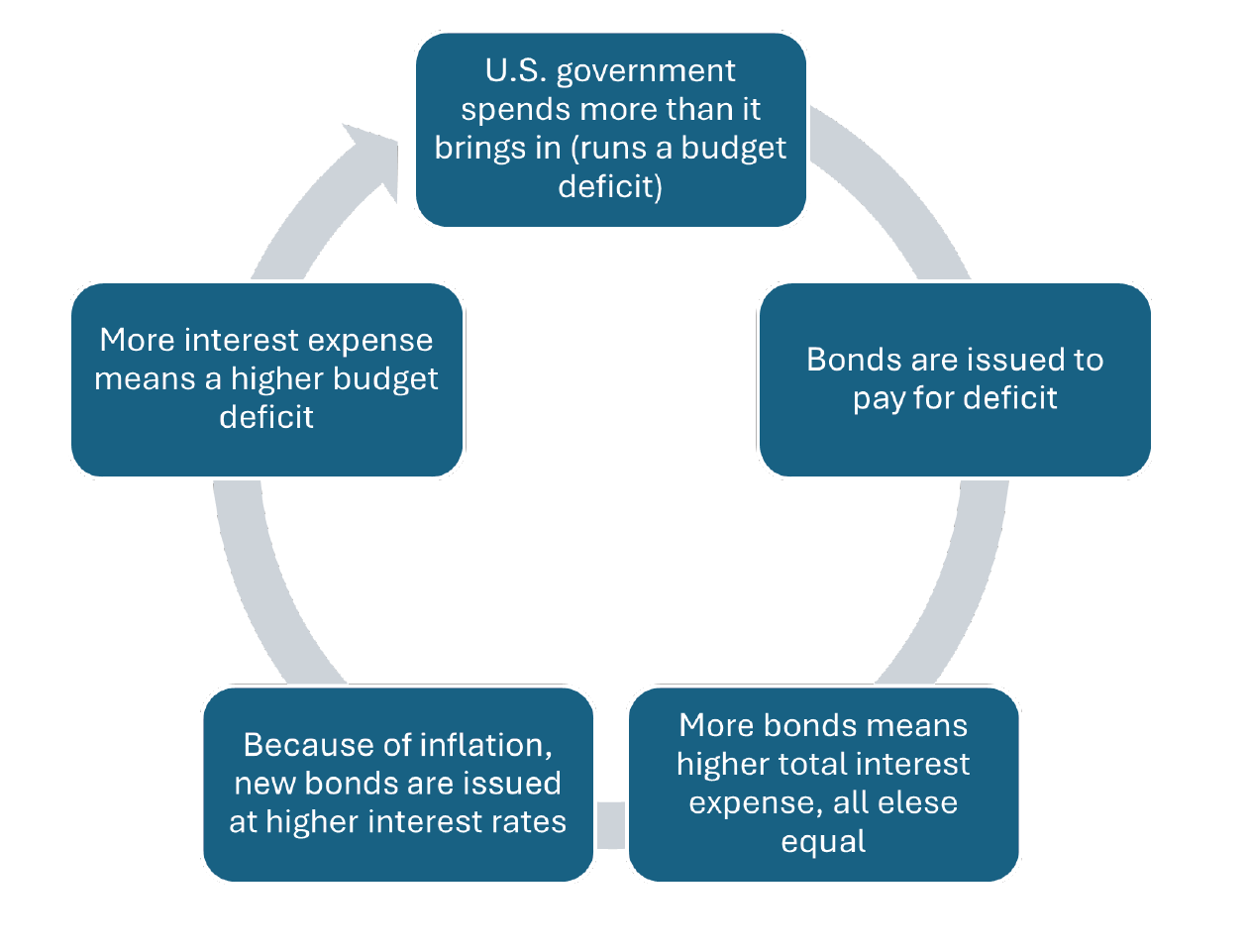

All else equal, growing amounts of debt will lead to higher interest expense payments. This is a problem because debt is becoming an increasingly large government outlay that, without changes to fiscal policy, will require more debt issuance simply to pay the interest expense.

Growing national debt is expected to increase interest expense outlays as % of GDP6

For the first time ever in 2024, interest expense on U.S. federal government debt held by the public surpassed $1 trillion. It is the second largest expenditure and set to become the largest.7

5Department of Treasury. Debt held by the public. Based on quarterly data through April 2024.

6Congressional Budget Office. The Budget and Economic Outlook: 2024 to 2034. Published February 2024.

7U.S. Bureau of Economic Analysis. September 2024.

FEDERAL RESERVE: MONEY PRINTING, INTEREST RATES, AND INFLATION

The next important player in this story is the Federal Reserve (the “Fed”). In its own words, “the Federal Reserve System has been given a dual mandate, pursuing the economic goals of maximum employment and price stability. It does this by using a variety of policy tools to manage financial conditions that encourage progress toward its dual mandate objectives—in other words, conducting monetary policy.”8

Following the great financial crisis in 2008, the Fed, through a process called Open Market Operations, brought interest rates to zero and implemented emergency spending programs. Initially, the goal was to stabilize the economy. However, it maintained rates near zero and continued spending programs despite a strong economy. The result: a significant increase in the money supply, inflation, and dollar debasement.

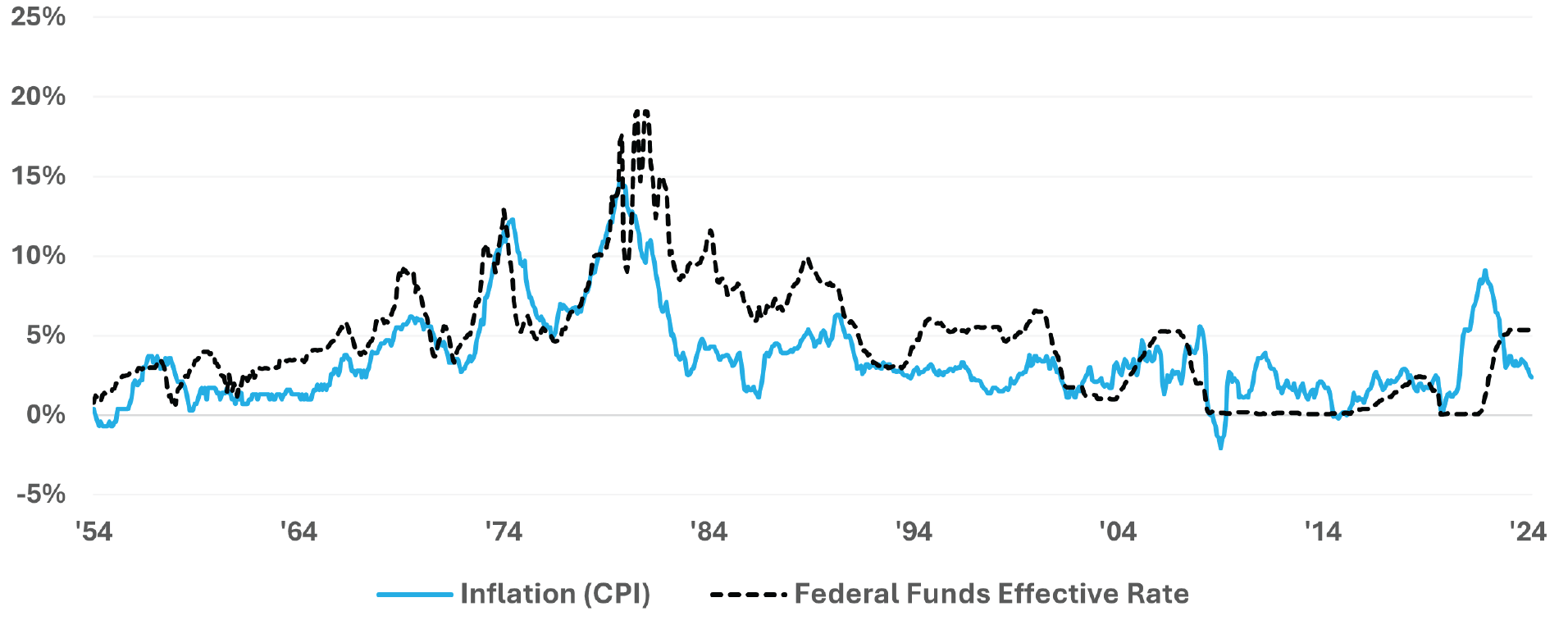

The Fed held interest rates near zero following 2008 until inflation hit 40-year highs9

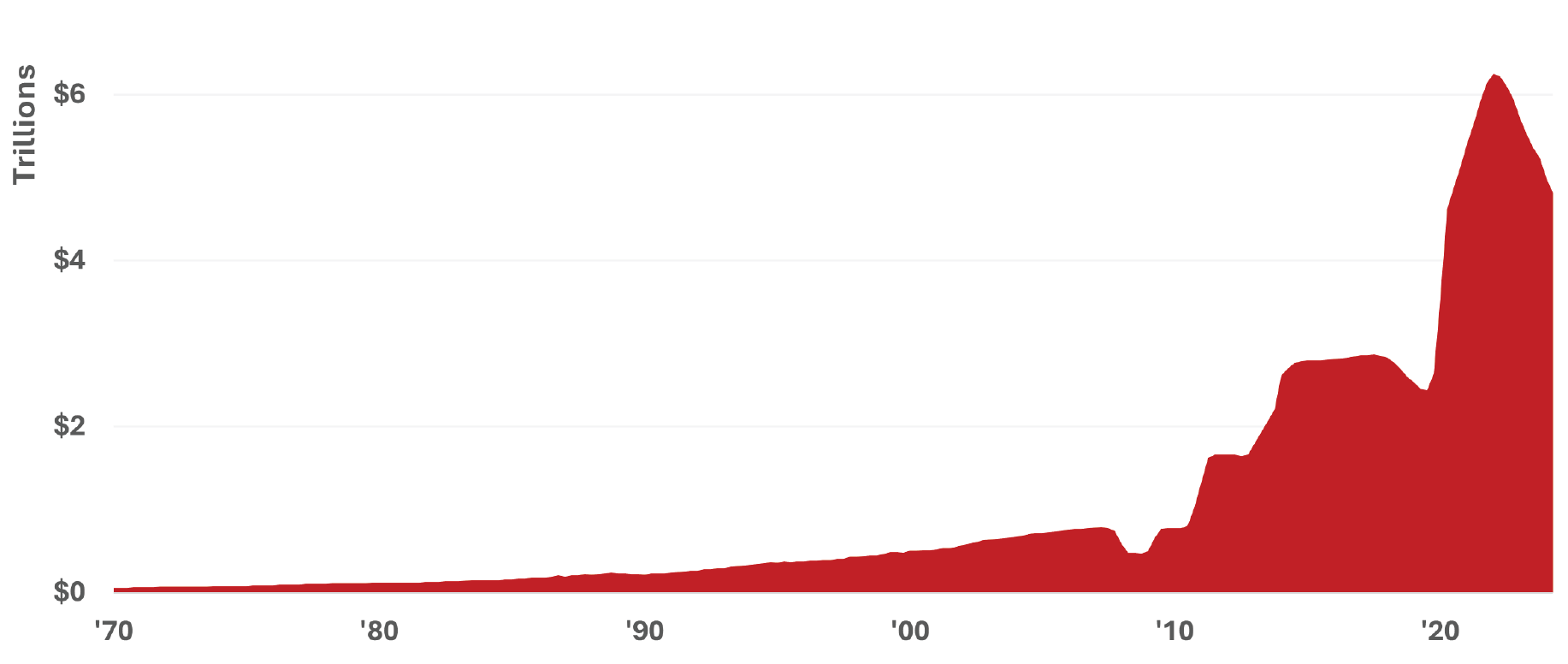

The Fed’s holdings of federal debt peaked at over $6 trillion in 202210

8St. Louis Federal Reserve Bank. The Fed and the Dual Mandate.

9Bloomberg LP. OECD. Federal Reserve Bank of New York. October 2024. The effective federal funds rate (EFFR) is calculated as a volume-weighted median of overnight federal funds transactions reported in the FR 2420 Report of Selected Money Market Rates.

10U.S. Department of Treasury. September 2024.

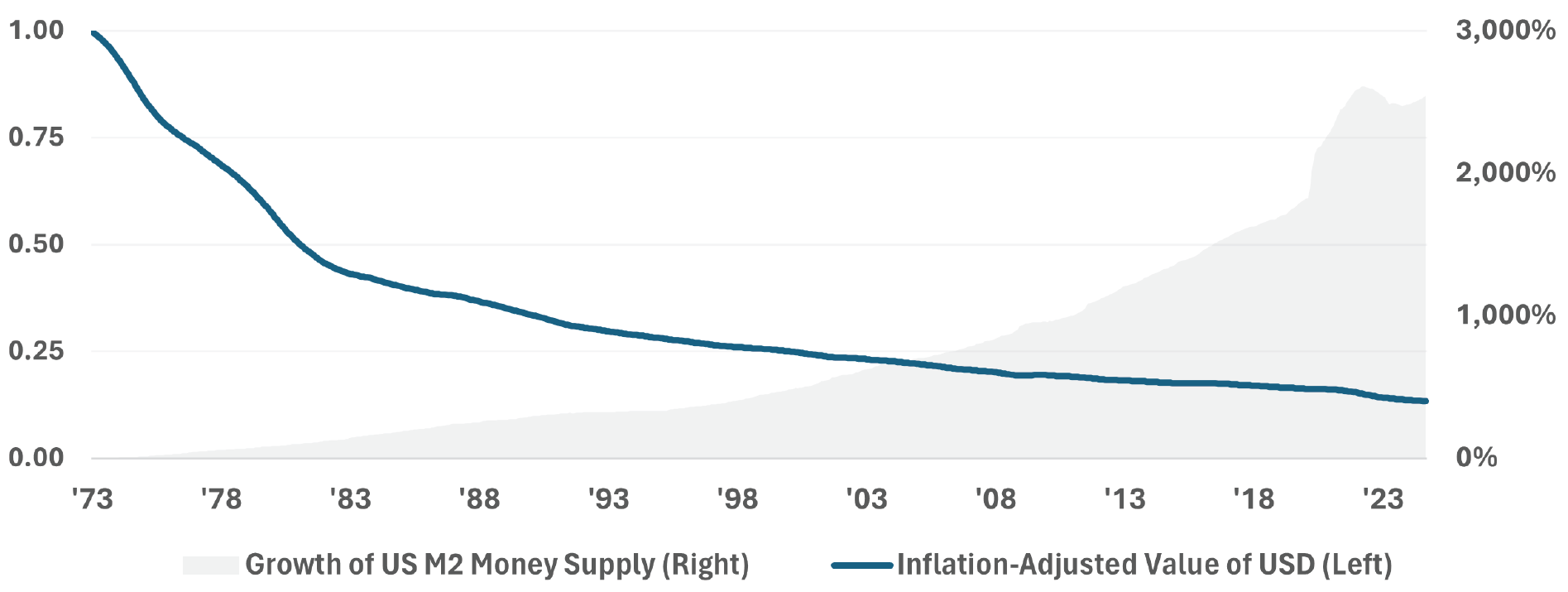

The Fed’s actions ballooned the money supply and eroded the value of the dollar11

The M2 money supply is a measure of the total dollars in cash deposits and other deposits readily convertible to cash, such as money market funds. The Fed’s actions since 2008 significantly inflated the M2 money supply, growing it 159%. From 2020 to 2024, the M2 money supply grew by 38%. When all this money enters the financial system, the value of the dollar erodes in a process called dollar debasement. This is why a dollar today is worth only $0.13 of a dollar in 1973.

Another consequence is inflation. Following a 40-year high in inflation in 2022, the Federal Reserve was required to enter one of the steepest interest rate hiking cycles in history. Interest rates went from zero to over 5%. A consequence was that the new debt issued by the federal government was done at much higher interest rates.

The U.S. federal deficit has created a self-perpetuating debt cycle

11Bloomberg LP. Board of Governors of the Federal Reserve. OECD. September 2024.

DECLINING DOMINANCE OF THE U.S. DOLLAR

Thus far, the U.S. has survived the self-perpetuating debt cycle because of the dollar’s status as the world’s reserve currency. This status carried over from the Bretton Woods era post-1973 and was maintained because of the United States’ standing as an economic and military leader with political stability. Essentially, the U.S. dollar has been perceived as a safe and stable currency for which the

world can conduct trade and financial transactions. Yet, the U.S. dollar’s status as the world’s reserve currency continues to decline in a process known as de-dollarization. The most used benchmark of the U.S. dollar’s status, known as the percentage of total foreign exchange (“FX”) reserves, reveals that the dollar dropped from 71% of reserves in 1999 to just 58% in 2024.12

Despite its dominance, the U.S. dollar as a % of FX reserves continues to drop13

There are two themes underlying the decline in the U.S. dollar. The first is the decline in the perception of the stability of the U.S. dollar and the political system that backs it. The second is a natural movement to alternative systems which better facilitate trade and transactions. In this paper, we focus on the first.

From a geopolitical perspective, the U.S. government has shown its willingness to weaponize the U.S. dollar. Following Russia’s invasion of Ukraine in 2022, the U.S. Department of Treasury’s Office of

Foreign Assets Control disconnected several Russian banks from the international financial system backed by SWIFT. These banks conducted approximately 80% of their $46 billion of foreign exchange transactions in U.S. dollars.14 Other adversaries of the United States have been threatened with the same. Despite a country’s relationship status with the United States, this type of action raises concerns about the viability of the U.S. dollar and has led many central banks to seek out alternatives, including gold.

12IMF COFER.

13Bloomberg LP. IMF COFER. September 2024.

14U.S. Department of Treasury Press Release. U.S. Treasury Announces Unprecedented & Expansive Sanctions Against Russia, Imposing Swift and Severe Economic Costs.

Central banks increased quarterly purchases of gold following dollar weaponization15

In 15 years, foreign investors went from holding almost 50% of the total U.S. debt held by the public to just 30%16

The growing debt problem in the United States raises a lot of concerns. It is uncertain how these levels of deficits and debt can be maintained, especially if inflation requires interest rates to go up. The world’s reserve currency status made U.S. federal debt and attractive option for foreign purchasers. Yet there is a growing trend where foreign

and international investors are becoming a smaller fraction of total public holders of U.S. federal debt. It should come as no surprise that dollar devaluation via money printing is the result, at least in the short-term where there are enough willing buyers of U.S. federal debt.

15Bloomberg LP. Quarterly demand (net purchase) data. June 2024.

16U.S. Department of Treasury. April 2024.

LOOK TO GOLD AS A SOLUTION TO A DECLINE IN THE U.S. DOLLAR

Gold has served as mankind’s most enduring form of money for millennia and has always played an important role in the international monetary system. It was the basis for the value of the U.S. dollar and foreign currencies prior to the end of the Bretton Woods System in 1973.

Gold’s unique attributes have well positioned it to play this role. Beyond its physical properties as a precious metal, scarcity is one of the most important attributes in terms of its enduring value.

Only 244,000 metric tons of gold have been discovered today, including 57,000 metric tons underground; a simple container 23 meters on each side could hold all the gold discovered thus far.17

Gold cannot be turned into a money printing machine. Unlike the U.S. dollar, gold is not backed by debt and has maintained its purchasing power during periods of inflation. Gold’s value is derived independent of the holder or counterparty, and it is not able to be manipulated for political purposes.

As the value of the dollar erodes from poor fiscal policy and de-dollarization, Gold has already demonstrated its value18

Even after adjusting for the impact of inflation, $1 worth of gold in 1973 is now worth over $5 while the value of $1 in 1973 is only worth $0.13 in 2024. In fact, except for a very brief period in 2001, the inflation-adjusted value of gold has always been higher than it was in 1973, demonstrating its resilience as a hedge against inflation.

Gold is at record highs and strong trends are already underway that should serve as tailwinds for

the price of gold. Without any meaningful change in U.S. fiscal policy, which seems unlikely as we sit here in 2024, the price of gold could continue to skyrocket. Investors have several choices when it comes to accessing gold. Investors can leverage their gold exposure to also generate a yield by combining a gold overlay with other income-producing strategies. This approach allows investors to access gold while putting their money to work in strategies that can regularly pay them now.

17U.S. Geological Survey. How much gold has been found in the world?

18Bloomberg LP. OECD. September 2024.